Calgary’s Office Market Has a Second Act. Not Everyone Noticed.

For much of the past decade, Calgary has been cast as the cautionary tale of the North American office market.

At one point, nearly one-third of the city’s downtown office space sat empty—an extraordinary figure for a major business district. Tower after tower built for a booming energy economy suddenly found itself without tenants. In the years that followed, Calgary became a case study in urban adaptation, with empty office buildings steadily converted into apartments, hotels, and classrooms.

The narrative is familiar by now: offices are dying, and cities must reinvent themselves as places to live rather than places to work.

It is a compelling story. It is also only half true.

The Quiet Shift

Beyond the headlines about office-to-residential conversions, a quieter shift is taking place in Calgary’s commercial property market. While many institutional investors have largely abandoned acquisitions in the sector, a small group of well-capitalized local landlords are moving in the opposite direction. They are buying office buildings at prices that would have been unimaginable a decade ago and optimizing them.

In a market that many observers have already written off, they see something different: an asset class that has already been brutally repriced.

The Full Weight of the Problem

To appreciate why this strategy is gaining traction, one must understand the scale of Calgary’s office market and the depth of its downturn. Downtown Calgary contains roughly 43 million square feet of office space, making it one of the largest central business districts in North America relative to population.

The collapse of global oil prices in the mid-2010s forced energy companies—the traditional anchor tenants of Calgary’s skyline—to shrink, merge, or disappear altogether. Corporate consolidations reduced the number of headquarters occupying large blocks of space. The result was an extraordinary surplus of empty desks in a city that had spent decades building towers for a booming industry.

Then came 2020. Oil prices went negative in April of that year. Then the pandemic accelerated the global shift toward hybrid work almost overnight. In a city accustomed to boom-and-bust cycles, Calgary’s office furniture market took one look and said, “hold my beer.”

The consequences didn’t stop there. As energy companies continue to merge and consolidate today, they routinely return excess space to the market through subleases. High quality, attractively priced inventory creates “shadow vacancy” for older buildings trying to compete for the same tenants. Vacancy has remained stubbornly in the high-20-percent range ever since.

Very few cities have experienced such a dramatic reversal.

Many Lenders are Overexposed

Financing remains a major hurdle. After years of falling values, many lenders are still overexposed to Calgary office properties and have little appetite for additional risk. Their only option is often to roll over existing loans, frequently ignoring Loan-to-Value and Debt Service Coverage ratios while plugging their noses. Credit departments endure cataracts and severe indigestion as they crunch the numbers, with extended amortization serving as their long-term strategy. With so little debt liquidity, offloading this exposure at scale remains impossible. The industry has coined this strategy as “extend and pretend.”

Policy Steps In, Encourages Conversions

Faced with that reality, Calgary’s policymakers responded with unusual ambition. The city launched one of the most aggressive office-to-residential conversion programs in North America, offering incentives of up to $75 per square foot to transform obsolete office towers into housing. More than twenty projects have now been approved, removing approximately 2.7 million square feet of office space from the downtown core, adding more than 2,600 residential units.

The program has attracted international attention, and rightly so. Conversions are bringing life back to a downtown that once emptied out after business hours, pumping millions of dollars back into the local construction industry.

Even Successful Policies Have Limits

The buildings best suited for conversion—the ones with the right floor plates, window spacing, elevator cores, and mechanical systems have largely been identified. What remains are buildings that still work as offices and those older, inefficient properties. They are often poorly located or functionally obsolete.

For some of them, operating cost slippage creates negative income. When that happens, the land beneath the tower can become more valuable than the building itself. That math is never good if you’re trying to avoid a date with the wrecking ball.

This opportunistic disparity has investors examining something different. Instead of asking which buildings can be converted, they’re increasingly asking: which ones are worth saving?

More than twenty projects have now been approved, removing approximately 2.7 million square feet of office space from the downtown core, adding more than 2,600 residential units.

Significant Repricing Changes the Economics

For a growing number of entrepreneurial landlords, the answer lies in the extraordinary repricing that has already occurred. During the peak of the energy boom, downtown A and B class office buildings often traded for more than $400 per square foot. Today, after years of falling rents and persistent vacancy, similar assets can sometimes be acquired for $50 to $90 per square foot.

At those prices, the economics of ownership look very different.

The strategy being pursued by these investors is neither flashy nor particularly complicated. It relies less on financial engineering than on operational discipline. Buy well-located but underperforming buildings. Invest in the right upgrades. Pursue tenants aggressively. Gradually rebuild occupancy.

In real-estate jargon, it is known as a buy-and-optimize strategy.

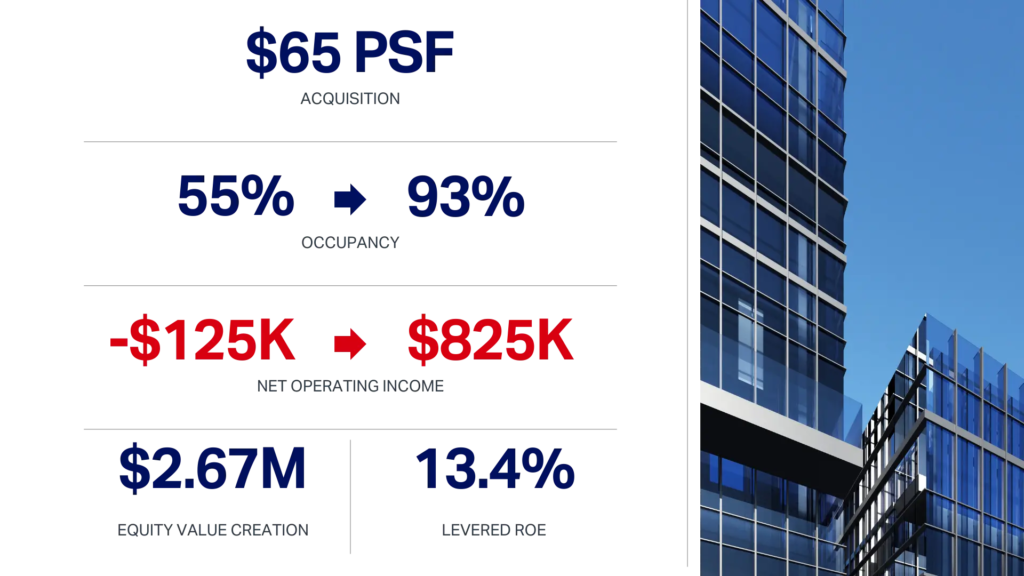

The financing ‘stat line’ here is a framework consistent with the base assumptions derived from recent acquisition financing arranged by Canada ICI for office assets in Calgary.

Key Assumptions:

- The stabilized valuation is based on an 9.00% exit cap rate taking the value from $65 per square foot to over $100 per square foot.

- Tenant Inducement and Commissions were assumed at $50 PSF

- Active management of the asset slashed ‘operating cost slippage’ from $675,000 to $105,000.

- Assumes no increase in the average rental rate

Opportunity for the Nimble Investor

As it often happens, the caution of institutional lenders creates an opportunity for smaller, more nimble investors. Many private groups acquiring office buildings today are operating with large equity cushions, sometimes contributing 60 to 70 percent of the purchase price while maintaining substantial reserves for leasing incentives and capital improvements.

That flexibility allows them to make decisions and compete for tenants that highly leveraged owners simply cannot. Seasoned local investors have something many institutional landlords lack — boots on the ground worn by years of experience. Years of operating in Calgary have given them deep relationships with brokers, tenants, and contractors, allowing them to spot deals early, line up tenants quickly, and navigate the small details that rarely show up in market reports.

They also move faster. Without layers of investment committees or rigid mandates, local owners can structure creative leases, tailor spaces to specific tenants, and pivot as conditions change. In a market like Calgary’s—where relationships often matter as much as rent—those advantages can turn a struggling office building into a surprisingly resilient one.

Just as important, they understand that competing solely on price is no longer enough. Calgary’s office market, like many others, is increasingly defined by a flight to quality. Tenants are gravitating toward buildings that offer something more than rows of desks and fluorescent lighting.

Landlords who recognize this shift are transforming their properties accordingly.

During the peak of the energy boom, downtown A and B class office buildings often traded for more than $400 per square foot. Today, after years of falling rents and persistent vacancy, similar assets can sometimes be acquired for $50 to $90 per square foot.

Reimagining the Office

Food halls, fitness centres, sports courts, golf simulators, and hospitality-style collaboration spaces are some institutional landlord strategies. The goal is not merely to offer cheaper office space, but to create an environment where employees want to spend time.

In the hybrid-work era, the office must compete with the comfort of home and justify its existence every day.

When the formula works, the results can be striking. Buildings that were once half empty have in some cases been stabilized at occupancy levels exceeding 95 percent. Because the assets were acquired at such deeply discounted prices, the resulting returns can be unusually strong, generating unlevered double-digit returns in a property sector most classify as Calgary’s real estate recycle bin.

Seen from this perspective, Calgary’s office market looks less like a permanent casualty of economic change and more like a market that has already absorbed most of its correction.

Rents have been depressed for years. Property values have fallen dramatically. Millions of square feet of office space are being removed through conversions. Few commercial real-estate markets offer investors such a clear sense that the painful repricing may already be behind them.

The real risk now is stagnation.

When the formula works, the results can be striking. Buildings that were once half empty have in some cases been stabilized at occupancy levels exceeding 95 percent. Because the assets were acquired at such deeply discounted prices, the resulting returns can be unusually strong.

Buildings Worth Saving

Owners who continue to hold underperforming buildings without a credible strategy face harsh arithmetic. As operating costs rise and rental income stagnates, asset values can eventually fall below the value of the land beneath them. When that happens, demolition becomes the only rational outcome.

Yet for buildings with the right fundamentals—prime locations, Plus-15 connections, and flexible floor plates—the future looks a lot brighter. With the right mix of capital, discipline, and perseverance, even distressed buildings can become stable, long-term assets.

Downtown reinvention doesn’t happen overnight. It happens lease by lease, floor by floor, deal by deal. Calgary’s office market has recalibrated. It still has life and the towers that once symbolized uncertainty are quietly anchoring a comeback.

There’s no magic here, no revolutionary idea. Just grit, experience, and dusty boots worn in the trenches. Rebuilding rent rolls one deal at a time, solving problems as they come in the door, and knowing what it takes to get a deal done because you’ve been there before.

That’s how “maybe this will work” becomes “look what we did.”

Will Industrial Rents Surpass Retail Rents?

David describes the unprecedented changes in the industrial asset class and how these changes were a...

Building a Safer, Smarter and Sophisticated ICI

Technology is converging on every industry. What about commercial real estate? Bob Troppmann discuss...

Related Articles