Commercial Real Estate in the Time of COVID-19

These days, uncertainty is about the only thing we can be certain about. While inboxes are flooded with circulars from organizations keeping us informed regarding changes to their policies, what’s missing is a discussion of the real impact on both borrowers and lenders. Below, we’ve summarized how we think the pandemic will impact Canada’s economy and affect future CRE lending.

1. Sentiment

In light of the significant disruptions to business around the country due to COVID-19, what is the current sentiment in the Canadian mortgage market?

The sentiment in the business community toward the Canadian mortgage market started shifting quickly during the week of March 9. Since then, we’ve seen a retrenchment of capital as lenders across the spectrum, from institutional capital to private funds, pivot towards a defensive posture. Ten-year Government of Canada (GOC) yields fluctuated as much as 50 basis points from peak to trough, and Bank of Canada key interest rates were slashed by 100 bps.

Commercial mortgage lenders across the country reacted and changed their focus to several key priorities including the following:

- Stress testing portfolio and borrower capacity and liquidity

- Managing lending and servicing platforms that can operate in a remote environment

- Working to stabilize volatility in both their pricing models while also managing potential disruptions to internal capital supply.

The Canadian mortgage market is extremely cautious at the moment and this will continue until the market regains its footing. Lender activity continues by processing pre-existing loan applications, and managing active portfolios.

2. Deferrals

Are lenders offering mortgage deferrals?

The general answer to this question is that requests are being evaluated on a case-by-case basis. Positions on deferral requests vary widely and are directly related to how each mortgage fund is capitalized, and also impacted by how much support the lenders receive from levels of government. To evaluate mortgage amendment requests, borrowers were asked to provide the following information:

- Demonstration of hardship at the asset level including negotiated terms with tenants

- Proof of hardship at the sponsorship level

- Updated rent roll and operating statements for all properties owned by the borrower and for the guarantor(s)

- Financial statements of the borrower including year-to-date operating statements

- Financial statements of the guarantor(s)

- Bank statements for borrower, shareholders, and guarantors.

How does a deferral impact my loan?

There’s a difference between a deferral and forgiveness. Lenders agreeing to adjust mortgage payments are NOT forgiving principal or interest. In some circumstances, they agreed to defer interest or both principal and interest with the understanding that these amounts will be capitalized and added to the existing loan.

How is the CMHC viewing mortgage deferrals?

On March 23, the Canada Mortgage and Housing Corporation (CMHC) announced they would permit all approved lenders to defer up to six monthly mortgage payments of principal and interest for “borrowers impacted by COVID-19.”

National Housing Act’s (NHA) Mortgage-Backed Securities are investments that are backed by pools of insured mortgages in which payment of NHA MBS principal and interest is guaranteed by the Canada Mortgage and Housing Corporation (CMHC).

NHA MBS issued under the program use the modified pass-through approach. That is, when borrowers fail to make timely payments on their loans, the issuer ensures that the necessary funds are available. CMHC guarantees that monthly payments are made to investors. If there’s any failure, delay or default under the terms of the certificate, the issuer is responsible and liable for such failure, delay or default. The investor then has the option of recourse to CMHC.

While we at Canada ICI don’t foresee any issuers becoming insolvent because of all the mortgage relief requests during these early days, rest assured it’s all hands on deck. When a borrower makes a deferral request to their lender (remember CMHC is the insurer), consider that the lender is receiving a deluge of claims, almost simultaneously. Lenders are processing each deferral claim with scrutiny and due diligence to triage the ones most in need.

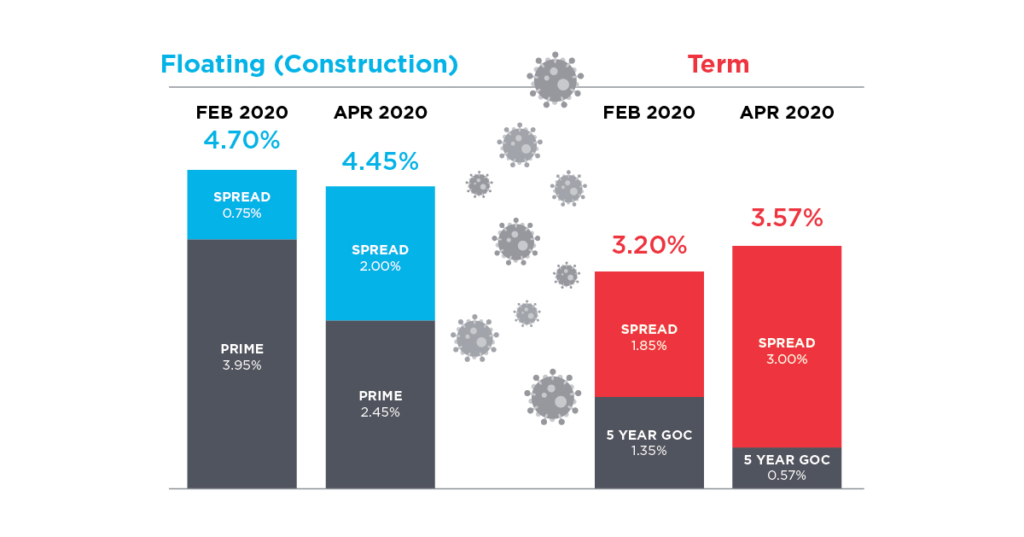

3. Pricing

What impact has COVID-19 had on pricing?

The lenders that remain active in this COVID-19 environment are price-making and we’ve seen an uptick in spreads. This has been counterbalanced with index yields like the Chartered Bank Prime or Government of Canada yields that have decreased over the last 30 days.

Effective borrowing rates for the remaining available capital are fairly consistent compared with where the rates were pre-crisis. This is subject to change as capital may become more limited. A large portion of the mortgage market is pausing underwriting new business at this time because lenders are experiencing difficulties with the following:

- Assessing the market due to a lack of evolving data points

- Managing capital calls and redemptions

- Competing for capital internally and externally with alternative investments.

4. Capital

Will capital be available for my real estate financing needs? In short, the answer is “yes.”

Many institutions have been provided liquidity from the federal government, which mandated financial institutions maintain capital outflow. We still have several investors in term and construction segments, notwithstanding recent developments. We are encouraged by the amount of capital flowing into the system.

5. Expectations

What can I expect as a borrower today?

Our experts have shared their experiences in weekly internal communication. There are some recent changes borrowers should prepare for, including:

- More balance sheet scrutiny

- More supporting information requests on a borrower’s Net Equity Position –post-COVID

- More lenders passing on deals

- Longer credit approval processes

- Less risk appetite resulting in lower loan-to-value (LTV) and loan-to-cost (LTC) ratios

- Inconsistent pricing models

- Deals requiring higher yielding sub debt that wasn’t required before.

We have heard a lot about “the new normal” with COVID-19 and we’ve thought about what that means for our clients. While we don’t have a crystal ball, we know two things are certain: We will stabilize and we will remain at the centre of financing from peak to trough.

As the pandemic continues, some of the perspectives in this post may fall out of date. This blog post reflects our views as of April 13, 2020.

The Fourth “C” of Credit – COVID

The effects of the coronavirus on the other three c's (collateral, cash flow, and credit) have been...

Transacting in the Midst of COVID-19

Canada ICI was able to arrange a ~$288mm Construction Loan on behalf of one of Toronto's leading dev...

Related Articles